The SpaceX IPO Is Not an Investment. It's a Lottery Ticket.

Why I'm sitting out the biggest IPO in history despite the massive hype.

Everyone is talking about SpaceX SPCX 0.00%↑ right now. The biggest IPO in history. The company that put a car in orbit and is going to supposedly ‘colonize Mars’.

IPO = initial public offering.; the first time a company is listed on the stock market and is available to the public

I’ll be honest: when something gets this much hype, my first instinct isn’t excitement. I tend to believe to stay away from IPOs because they generally perform poorly. For instance, IPOs have historically underperformed the rest of the market over time. The only exception was in 2021.

So let me walk you through exactly why I’m sitting this one out, and why a lot of retail investors are about to overpay for a dream.

The Numbers Don’t Support the Valuation

Let’s start with the S-1, because the prospectus tells you everything you need to know.

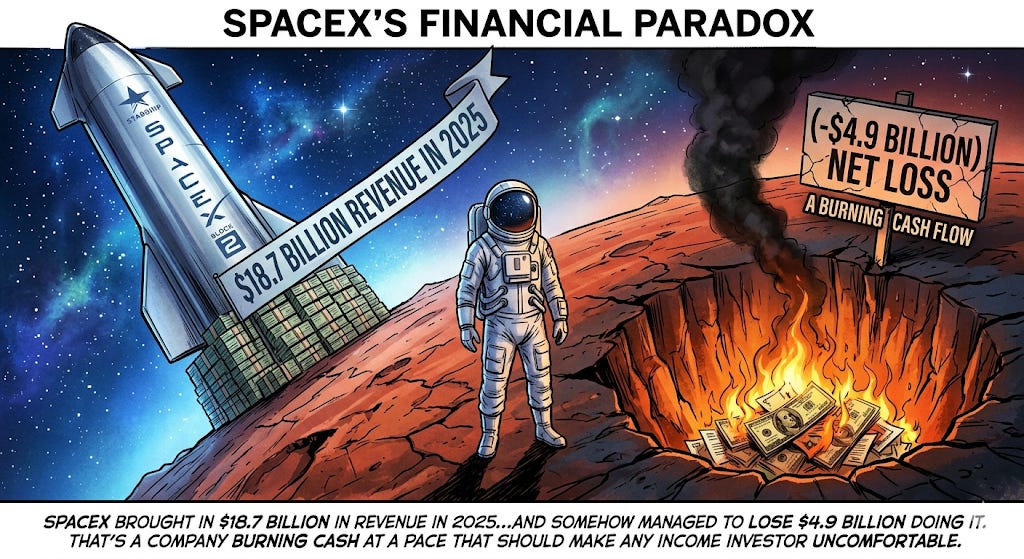

SpaceX brought in $18.7 billion in revenue in 2025 and somehow managed to lose $4.9 billion doing it.

The expected IPO valuation sits somewhere between $1.5 and $2 trillion. That puts SPCX at roughly 80 to 110x price-to-sales. Not price-to-earnings. There are no earnings. Price-to-sales.

For comparison, Netflix is a high-growth, widely beloved tech company that trades at a fraction of that multiple. When Saudi Aramco, arguably the most profitable corporation on Earth, went public in 2019, investors accepted a valuation of about 6x yearly sales. It still traded below its IPO price for years afterward.

SpaceX isn’t asking you to pay 6x sales. It’s asking you to pay 80 to 110x sales for a company losing billions.

Investing For What Could Be

So why would anyone pay that? The thesis boils down to one word: optionality.

The idea is that you’re not buying SpaceX the rocket company. You’re buying a stake in every massive business it might become: Starlink internet, direct-to-cell satellite coverage, AI data centers, Starship cargo missions, xAI and the Grok platform, and eventually a permanent human colony on Mars.

Just list to the pure energy and excitement in this video.

That last one isn’t a joke. Elon Musk’s performance pay package in the S-1 is literally tied to establishing a human settlement on Mars.

Look, I’m not here to tell you Starlink isn’t a real business.

It has over 10 million subscribers and is growing fast. That’s legitimate. But the S-1 projects a $28.5 trillion Total Addressable Market (TAM), a number so large it’s essentially meaningless.

For context, that figure is comparable to the entire volume of global payment transactions. When a company needs to claim the entire global economy as its TAM to justify its valuation, that’s a red flag.

The Anthropic Deal

One of the headline revenue items in the filing is a deal to rent compute capacity to Anthropic for $1.25 billion per month. On the surface, that sounds transformative. But buried in the details is a clause that should give every investor pause: either party can cancel with just 90 days’ notice.

That’s a handshake with a timeout. It cannot be relied upon as a durable revenue stream, yet the market will likely price it in as if it were. Therefore, I wouldn’t be surprised to see positive momentum at first.

You Don’t Own What You Think You Own

Here’s the governance reality that most retail investors won’t bother reading: Elon Musk controls 85% of the voting power.

No matter how many shares you buy, you have no meaningful say in how this company is run. Musk is effectively unfireable. He can cross-pollinate business decisions across Tesla TSLA 0.00%↑, Neuralink, xAI, The Boring Company, and SpaceX, and you have zero recourse as a shareholder.

The S-1 also discloses that SpaceX purchased 1,300 Cybertrucks at full MSRP from Tesla.

You read that right. The company losing $4.9 billion a year bought over a thousand electric pickup trucks from its CEO’s other company at full retail price while preparing to ask the public for money.

It Will Probably Pop on Day One. That’s the Trap.

Here’s the part that’s easy to miss: I actually think this IPO will have a strong debut.

SpaceX is only floating 4 to 5% of shares at IPO.

Float refers to the number of a company’s shares that are available for the general public to buy and sell on the open market, excluding locked-in shares held by insiders, founders, and major institutional investors.

The float is tiny. Demand from institutional investors and Musk loyalists will be enormous. Lock-up periods will keep insiders from selling. All of that creates upward price pressure regardless of the underlying financials.

This is textbook IPO mechanics. A small float plus massive demand equals a pop. That pop then gets covered breathlessly by financial media, retail investors pile in, and insiders eventually unlock and sell into that enthusiasm.

We’ve seen this movie before. It doesn’t usually end well for the people who bought tickets after the opening weekend.

If You Want Space Exposure, There Is a Better Way

Here is what frustrates me about the SPCX hype: investors who genuinely believe in the future of space connectivity are being handed a $2 trillion valuation and told to take it or leave it. You don’t have to.

Earlier this year, I issued a buy alert on AST SpaceMobile ASTS 0.00%↑, a company building the world’s first space-based cellular broadband network that connects directly to standard smartphones. No dish. No special hardware. Just your existing phone, connected via a satellite acting as a cell tower in Low Earth Orbit.

The contrast with SpaceX couldn’t be sharper:

ASTS has already validated the technology, making the first-ever 5G call from space. It has secured over $1 billion in contracted revenue commitments from partners like AT&T T 0.00%↑ and Verizon VZ 0.00%↑. It carries $3.2 billion in pro-forma liquidity on its balance sheet. And it is doing all of this at a fraction of the valuation SpaceX is demanding.

Since my buy alert, ASTS is up over 34% and has outperformed both the S&P 500 and the Nasdaq.

For the full ASTS breakdown including my valuation model and price target, check out the original article here.

I am not saying ASTS is risk-free. Launch cadence is a real variable, and space is hard. But when I am comparing a company asking 80 to 110x sales with zero earnings against a well-funded infrastructure play with real contracts and validated technology, the choice becomes clear to me.

If space is the future you want to invest in, you should be paying a fair price to get there.

What Dividend Investors Should Actually Do

None of this means space is a bad business or that Starlink won’t be massive. It might be. But there’s a difference between an interesting company and a good investment at a given price.

At 80 to 110x sales, with billions in annual losses, a CEO who answers to no one, and a float engineered to create artificial scarcity, SPCX is not priced for investors. It’s priced for speculators.

My portfolio is built on cash flow. Companies that pay me every month whether the stock goes up or down. That income compounds, it’s predictable, and it doesn’t require a Mars colony to materialize.

SpaceX might be the most fascinating company in the world. But I’m not buying a story at $2 trillion. I’m letting the hype cycle run its course. If in 12 to 18 months the business has matured, earnings are visible, and the valuation has come back to earth, then we can have a real conversation.

Until then, I’ll keep collecting my dividends and buying high quality growth positions.

Always do your own due diligence before making any investment decision. This is not financial advice.

Thanks for your insight!

Musk is a corrupt liar cheater felon tax cheat. He is not smart, but he is an incredible cheat and felon. He is anti American anti women, anti minorities. He is a cancer a syphilis a disease. Deport him and seize his assets